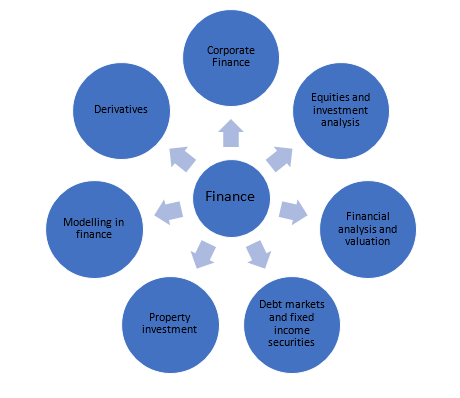

Finance, most simply put, is the study of money, banking, credit, investments, assets and liabilities through financial statements. These statements include balance sheets, cash flow statements, etc. and are produced as a result of accounting activities. Finance plays an integral role in the machinery of any organization, be it a start-up or a multinational corporation. Finance assignments help students understand asset management, auditing, tax and leverage management, and thus, the making of cost-based decisions. Students often need finance assignment samples for case studies and reports, which are the most common among finance assignments. Finance courses broadly cover the topics depicted in the below image.

A degree in finance can open doors to a plethora of opportunities out there, like banking, mortgage broking, credit analysis, insurance, and international finance. But the number of students in line for the cream of the crop jobs are high and thus, bagging an opportunity is not easy. There is no need to mention the role good grades play here. Gone are the days when cramming for the final exam used to be sufficient. Academic curriculums of the modern world test students on a regular basis and the workload has multiplied manifold, forcing students to hire online finance assignment help in Australia.

Why Pick My Assignment Services?

My Assignment Services has been providing commendable services for finance assignment help since the last decade. We have a large team of finance assignment experts who are mostly Ph.D. degree holders or are ex-professionals in the industry. We can provide you with solved finance assignment samples as per your requirements, be it finance assignment sample pdf or word format.

Our financial management assignment experts have provided innumerable solutions in the past. They hold a comprehensive understanding of various standards as set by regulatory bodies like Australian Financial Security Authority, Auditing and Assurance Standards Board (AASB), Financial Reporting Council, etc. Our finance assignment solutions have scored maximum number of high-distinction grades. Some of the frequently asked topics provided by our finance assignment writing services are

- Corporate Finance

- Real Estate Finance

- Healthcare Finance

- Finance for International Business

- Finance & Quantitative Methods

- Financial Management

- Analysis of Financial Statements

- Accounting and Finance for Business

- Certificate IV in Finance and Mortgage Broking

Finance Assignment Sample

Check out the below finance assignment sample question which was recently solved by our experts.

Our Approach

Students can now stop sweating over google searches like ŌĆśpay someone to do my finance assignmentŌĆÖ or ŌĆśonline finance homework helpŌĆÖ and can share their workload with our experts. We provide finance assignment help at affordable rates.

The customer care executives at My Assignment Services are available 24*7 to address your concerns and queries. All your requirements will be efficiently communicated to the experts. In case you need guidance, we can provide one-on-one consultation sessions with our finance assignment help experts. We also provide:

- Initial draft of the assignment for the students to examine the solution and provide recommendations, if any.

- Multiple revisions until they are completely satisfied with the solution.

- Complimentary Plagiarism report to ensure plagiarism-free assignments.

- 100% authentic solutions.

- One-on-one expert tutorials.

- 24*7 customer service.