- Subject Code : HI6028

- University : Holmes Institute My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Taxation

Assessment

QUESTION 1

GOODS AND SERVICE TAX

Goods and service tax refers to as a value added tax. In Australia, GST is levied at a rate of 10% on most of the goods and services sold. This tax is charged on every stage of the transaction but is refunded to everyone present in this chain of transaction except the final consumer. The tax of GST is a consumption based tax that is the person consuming would be the one paying the tax. (GST)

All the businesses and the organization that are registered under the GST law will have to charge goods and service tax in the price for which they are offering the goods and services to the customer. Also they can claim credit of GST that has been included in the goods and services thereby for the purpose of enhancing and building their own business. (GST)

An organization registered under GST they should have registered for the same then whenever they sell goods and services in Australia they are taxable and have to pay goods and service tax to the government. In the case of nonprofit organization there are certain conditions that the government and the tax law have provided to them.

In the given case of the company the city sky who is paying fees to its lawyer for receiving legal services related to its business. The lawyer is charging a certain amount of fees from the company. The yearly income of the lawyer is $300,000 which is taxable under the law of the country. So the GST would be charged by the government on the services of the lawyer received by the company for its business use. The company is registered under the GST law and the services of the lawyer are charged under the scheme of Reverse Charge Mechanism so the GST which will be charged by the government will be paid by the company itself as on the basis of reverse Charge Mechanism Scheme. (When to charge GST (and when not to))

The City Sky Company would be making the payment to the lawyer and will also pay the GST on the amount paid to the lawyer. Reverse Charge Mechanism is a scheme in which the company which is registered under the GST would be entitled to pay the tax to the government if the services which are receiver are either partially or completely for the purpose of business.

In the above charge the company would pay the tax and the entitlement of getting the Input Tax Credit will also be held by the company. Input Tax Credit refers to the credit which the any person both real and artificial would receive after paying the tax over the services or things which are there for the purpose of resale. Here, the company is receiving the services of the lawyer for the construction of a number of apartments in a building which are to be sold to the public after completion. The services are received by the company for the purpose of the business and there is further sale involved of those goods for which services are received. (When to charge GST (and when not to))

The company would pay the tax in this year and in the next year the Input Tax Credit would be received by this company. As the tax is paid by the company on the behalf of the lawyer as per the scheme of reverse Charge Mechanism, so the entitlement of getting the benefit would also lie with the company as they are the payer. The government offers the benefit of the input Tax Credit only to that party who is paying the tax and bearing the pain of paying tax. If in this case the Credit is apportioned to the lawyer than this would be unfair as this would give the double benefit to the lawyer as he has not paid the tax that amount is saved and an additional credit of tax and on the other side the company will neither get the credit nor the benefit of not paying tax.

Hence, it could be concluded from report of the above case that the company is liable to pay the tax under the scheme of Reverse Charge Mechanism as the company and the lawyer both are registered under the law of GST. Further, as the tax is paid by the company so the entitlement of availing the credit of the paid tax also lies with the company. So it is concluded that these services are taxable as they are received wholly for the business and are completely taxable. The tax will be paid on the amount that is paid to the lawyer for his services. (When to charge GST (and when not to))

QUESTION 2

CAPITAL GAIN TAX

If an assessee sells his Capital Asset that might be real state or shares then the assessee will incur capital gain or capital loss on such sale made by him. The difference between the cost incurred in acquiring the Asset and the payout received by the assessee while selling or disposing of the Asset leads to such capital gains or losses for the assessee. All the capital gains have to be reported in the income statement and therefore the assessee has to pay capital gain taxes on such capital gains made by him during the financial year. It is considered that the capital gain taxes paid by him are the part of income tax that the assessee pays to the government. Whereas in the case of capital loss it cannot be claimed against any other income, it can only be used to reduce capital gains. (CGT assets and exemptions)

All the assets acquired after 20 September 1985 will be subject to capital gain taxes. There are following exceptions which include all the personal Assets of the assessee and the depreciating Assets will not attract capital gain taxes. Any car, home or personal assets such as furniture would not attract capital gain taxes. The capital gain applies not on the physical transfer of the Asset that is on the date on which the contract or the obligation has been admitted to fulfill. Also if you are an Australian resident capital gain taxes would be applicable to all your assets irrespective of their location that means wherever there are the capital assets in the world you need to pay capital gain taxes in Australia. (Calculating the cost base for real estate)

For all the capital gains that have happened in a financial year have to be reported in the same financial year. If there are both capital gains and losses in the same financial year then capital gain taxes have to be paid on the net gains arising in that financial year. For all the individuals and small businesses can generally discount their capital gains by 50% if the Asset has been held for more than one year. (Capital gains tax)

The treatment for shares in a company or units in a trust for the purpose of calculating capital gain taxes is done in the same way as all the capital assets are treated for tax purposes. The capital gains are applicable on the sale of shares in the case of an investor. For a person whose business is share trading and all the profit made by him in the sale trading of shares would be constituted as his own ordinary income and not capital gain. (Cost base)

For the purpose of acquiring at the cost of the Asset cost base formula which involves that all the costs associated with purchasing the Asset would be constituted together as the purchase price of the Capital Asset. The entire incidental cost of acquiring a capital gain tax asset which includes all the remuneration of the services paid to the broker, accountant etc. All the cost involved in the transfer including stamp duty fees, cost of advertising, making payments to the valuer other borrowing expenses. (Elements of the cost base and reduced cost base)

All the cost incurred over land Taxes, repairs and insurance premiums would only be included if the asset is purchased after 21st August 1991.

All the capital cost that has been incurred by the assessee in transferring or moving and asset for the purpose of increasing the value of the Asset are also included in the cost of Capital Asset.

In the case of collectibles capital gain tax are applicable whether the collectibles are kept for personal use for enjoyment they include paintings, drawings, photographs, sculpture etc. Also includes jewellery, antique items, and postage stamps. No capo applicable if the value of the collectible is less than $500 the collectible has been acquired before 16 December 1995. All the market value of the collectible when acquired by the assessee is $500 or below. (Working out your capital gain or loss)

The collectibles that has been acquired by an assessee and any capital losses that have incurred on the transfer/ sale of the collectible then and the capital loss can only be set off with the capital gain arising from the sale of the collectible. If in the current financial year there are no capital gains from the sale of collectibles then, the capital loss would be carry forwarded to the Future years. In the taxation laws of Australia there is no time limit for carry forwarding capital loss acquiring from the collectibles. (Shares, units and similar investments)

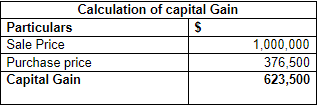

Sale of a block of land for $1,000,000:

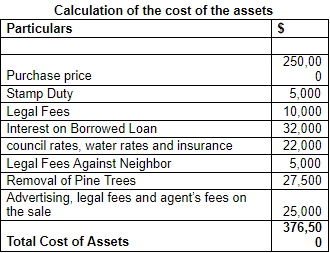

In this question asked Emma has purchased land in the year 1991 the purchase price was $250,000, over and above $5,000 incurred in stamp duty, $ 10,000 incurred in legal fees have to be included in the cost price of the Asset. Also the cost incurred free paying the interest of $ 32,000. Also as per the elements of the cost base all the taxes and insurance premium have to be included in the cost ways therefore $ 22,000 would also form part of the cost of the Asset. Since the cost of legal expenses incurred after 30th June 1989 therefore $5,000 will be included in the cost of the Asset. Also the cost incurred in the removal of pine trees and fees incurred in the sale of the land would also be included in the cost of the asset. (Modifications and interaction with other rules)

As per the question indexation has to be avoided therefore we will use discounting method.

50% of ($623,500) is $311,750.

Capital Gain taxes would be applicable on $ 311,750.

Sale of Emma’s 1000 shares in Rio Tinto for $50.85 per share:

Since Emma has purchased the shares before 19 therefore no capital gain taxes have to be paid by the on the sale of the shares made by her.

Sale of a stamp collection Emma had purchased, from a private collector, in January

2015 for $60,000:

Since the stamp collected by Emma would attract capital gain taxes as she purchased the stamps for $60,000 and sold them for $50,000 while increasing the auction expenses of $5,000. Therefore, capital loss of sale of stamps (50000-5000-60000) is $15,000. The loss incurred on the sale of collectibles can only be set off with the capital gains incurred on sale of collectibles. Otherwise if there are no capital gains then it will be carry forwarded in the future years. (Working out your capital gain or loss)

Sale of a grand piano for $30,000:

A piano was bought in the year 2000 by Emma for $80,000 and has sold the same for $30,000. As per the provisions of the law capital loss has been incurred but it can be observed that the piano was purchased for personal purpose and therefore no capital gains or losses in relation to a personal asset shall be included in the computation of taxes. Therefore there will be no capital loss for her in the financial year. (Modifications and interaction with other rules)

References

Calculating the cost base for real estate. (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/Calculating-the-cost-base-for-real-estate/

Capital gains tax. (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/General/Capital-gains-tax/

CGT assets and exemptions. (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/#collectables

Cost base. (n.d.). Retrieved from www.ato.gov.au: https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Cost-base/

Elements of the cost base and reduced cost base. (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-gain-or-loss/cost-base/elements-of-the-cost-base-and-reduced-cost-base/

GST. (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/Business/GST/

Modifications and interaction with other rules. (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-gain-or-loss/cost-base/modifications-and-interaction-with-other-rules/

Shares, units and similar investments. (n.d.). Retrieved from https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-investments/: https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-investments/

When to charge GST (and when not to). (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/Business/GST/When-to-charge-GST-%28and-when-not-to%29/

Working out your capital gain or loss. (n.d.). Retrieved from https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-gain-or-loss/

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start