- Subject Code : APC-309

- University : Sunderland University My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Accounting and Finance

Ans 3

i) Purposes of Standard Costing System:

According to Pagare (2020), Standard costing frameworks help in engineering endeavors and getting snippets of data into the conceivable effect of definitive choices on cost levels and points of interest. Standard expenses are used for:

-

Setting up money related plans.

-

Standardizing expenses and inspiration and evaluating efficiencies.

-

Advancing conceivable cost decay.

-

Streamlining costing approaches and empowering cost reports.

-

Assigning expenses to materials, work in cycle, and completed things inventories.

-

Trim the reason behind creating offers and contracts and at setting deals costs.

The plentifulness of controlling expenses relies strikingly upon an information on anticipated expenses. Rules fill in as appraisals which point out cost arrangements. Supervisors and chairmen become cost astute as they become mindful of results. This cost care will all things considered decline costs and empowers economies in all seasons of the business.

ii) Standard costing is a colossal subtopic of cost accounting. Standard costs are for the most part associated with a get-together alliance's costs of direct material, direct work, and collecting overhead (Pagare, 2020).

Makers, obviously, still need to pay the genuine costs. As prerequisites be there are regularly isolates between the guaranteed costs and the standard costs, and those abilities are known as changes. Standard costing and the connected changes are a fundamental affiliation device. On the inaccessible possibility that a flimsiness arises, the barricade becomes mindful that putting away costs have isolated from the standard (coordinated, anticipated) costs. If authentic costs are not actually standard costs the change is positive. An ideal change tells the supervisors that if the wide extent of various things stays obvious the true piece of elbowroom will likely beat the arranged good position.

Standard Costing is the second strategy of cost control (the first being the Budgetary Control) and is perhaps the most as of late created refinements of cost bookkeeping. The standard costing strategy has been presented in numerous ventures because of the restrictions of Historical Costing. In this way, it is essentially an after death of a case and has its own impediments.

CONTROL through norms and standard expenses is considered by Management to be an inventive program pointed toward deciding if the assets of the association are being utilized ideally or not. Standard expenses are typically decided during the budgetary control measure since they are helpful in setting up the adaptable spending plans and in assessing execution:

They help in setting practical costs and in distinguishing the creation costs that should be controlled examination of the real expenses with the standard costs gives us the difference.

Effectively dissected, different show how unfavorable propensities can be rectified. The current classification "Standard Costing and Variance Analysis" talks about the method of Standard Costing and Variance Analysis, which is focused on benefit improvement primarily by diminishing Materials, Labor and Overhead expenses (Pagare, 2020).

The strategy of standard costing can be relevant under specific conditions which can be given as follows:

-

There ought to be yield or creation of adequate volume of some standard item.

-

The techniques, tasks and cycles of creation ought to be fit for normalization.

-

The expenses ought to be equipped for being controlled.

Standard costing procedure can be applied effectively in each one of those ventures which are occupied with delivering normalized items and following cycle costing technique. Instances of such enterprises are: sugar, manures, concrete, footwear, bottling works and refineries, and so forth Public utility concerns like vehicle endeavors, power supply endeavors, waterworks, and so on, can likewise apply this strategy for controlling expenses and expanding proficiency. In jobbing enterprises and businesses delivering non-normalized items, this strategy can't be applied with advantage

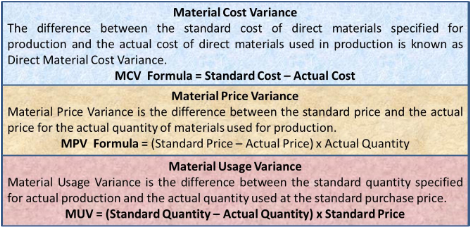

iii) Material Price Variance

According to Darmansyah, H. S. (2019). Material Price Variance is the capability between the standard cost and the authentic cost for the real proportion of materials utilized for creation. The reason behind material worth differentiation can be many recalling changes for costs, unprotected buying strategies, needs regard exchange, and so forth

Material Usage Variance

MUV = (Standard Quantity – Actual Quantity) x Standard Price

With the assistance of the above model, let us presently compute Material Usage Variance.

MUV = (200 – 150) x 10 = 500 (F)

The outcome is Favorable, since the standard amount is more than the genuine amount. In situations where the genuine amount is more than the standard amount, the outcome is in (A) which implies Adverse.

Wage Rate Variance

Work rate fluctuation is the distinction between genuine expense of direct work and its standard expense. The distinction because of genuine sum paid every hour and the standard rate while the time spends during creation stays as before.

The difference can be good and negative. Great when the genuine work cost every hour is lower than standard rate which implies the immediate work cost lower than anticipated. Then again, negative mean the genuine work cost more than anticipated.

Labour Efficiency Variance

Pleasant furniture fabricating organization presents the accompanying information for the period of March 2016.

Standard direct work rate every hour: $6.50

Real immediate work rate every hour: $6.75

Standard chance to deliver on unit of item: 3 hours

Creation during the period of March 2016: 600 units

Hours worked during the period of March: 1850 hours

Required:

Register direct work effectiveness difference.

Demonstrate whether the difference is positive or ominous.

Arrangement

Direct work productivity difference = (AH × SR) – (SH × SR )

= (1850 hours × $6.50) – (1,800 hours × $6.50)

= $12,025 – $11,700

= $325 negative

The difference is troublesome on the grounds that work worked 50 hours more than what was permitted by standard.

Then again, the change can be determined by utilizing figured recipe as follows:

Direct work effectiveness difference = SR × (AH – SH)

= $6.50 × ( 1,850 hours – 1,800 hours * )

= $6.50 × 50 hours

= $325 Unfavorable

*Standard hours permitted to make 600 units:

600 units × 3 hours = 1,800 hours

Note: The real immediate work rate isn't utilized to register this fluctuation.

References

Pagare, S. (2020). Standard Costing.

Drobyazko, S., Pavlova, H., Suhak, T., Kulyk, V., & Khodjimukhamedova, S. (2019). Formation of hybrid costing system accounting model at the enterprise.

Susi, M. C., Rahmat, S. T. Y., Semerdanta, P., & Darmansyah, H. S. (2019). Implementation of activity based costing system in real price calculation of cost of goods manufactured for the determination of the selling pricing for start-up business: fruit combining. Russian Journal of Agricultural and Socio-Economic Sciences, 94(10).

Remember, at the center of any academic work, lies clarity and evidence. Should you need further assistance, do look up to our Accounting and Finance Assignment Help

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start