- Subject Code : 7036EFA

- University : university of london My Assignment Services is not sponsored or endorsed by this college or university.

- Subject Name : Auditing and Assurance

Contents

Background of Hikma Pharmaceuticals

Nature, Purpose, Scope and Governance of Auditing within WorldCom and Hikma Pharmaceuticals

Critical Evaluation and Comparative Analysis of the role of Board of Directors, Governing Body and Internal Auditors of the two companies

Identification and comparison of accounting and internal control risks of the two companies

Audit Risk, Audit Procedures and Audit Evidence for Hikma Pharmaceuticals for the year 2019

Comparison of Audit Procedures of WorldCom and Hikma Pharmaceuticals

Limitations of Audit Report of WorldCom

The extending audit horizons

References

Background of Hikma Pharmaceuticals

Hikma Pharmaceuticals is a pharmaceuticals company headquartered in the U.K. that has its presence not just in the U.K. but also many other parts of the world. The company has been in existence for forty years now and has grown steadily as a leading global pharmaceutical business with a strong reputation for quality. The initial aim of the company was to establish a branded pharmaceutical sector throughout the area of the Middle East and North Africa (MENA). However, it acquired a generic pharmaceutical business in the United States in the early 1990s and established an injectable pharmaceutical operation in Portugal, expanding the company's outreach beyond the MENA region. The business has since continued to expand significantly through organic growth and acquisitions (Processing and Synthesis 2013). management”(Hayes, Gortemaker and Wallage, 2014)

Nature, Purpose, Scope and Governance of Auditing Within World Com and Hikma Pharmaceuticals

Nature

The main function of auditing is to lend credibility to the financial statements. The financial statements are the responsibility of management and the auditor’s responsibility is to lend them credibility. By the audit process, the auditor enhances the usefulness and the value of the financial statements, but he also increases the credibility of other non- audited information released by According to Darryl (2020), auditors should obtain fair assurance as to whether the financial statements as a whole are free of material misrepresentation, whether due to fraud or mistake and issue an auditor's report. However, fair assurance is a high standard of confidence but is not a guarantee that an ISA (UK) audit can always find information misstatement when it occurs (Accounting Tools n.d.). Misstatements may result from fraud or mistake and are considered material if they may reasonably be expected to affect the economic decisions made by consumers on the basis of such financial statements, individually or in the total (ACCA n.d.). However, even though the auditor is not able to provide an absolute assurance they are still required to provide a reasonable assurance that the audit will be able to detect any misstatements that are of material nature.

The audit of WorldCom was not successful in detecting any material misstatement even though there were so many material misstatements in its financial statements. The audit report provided an unqualified opinion even though the company went bankrupt soon after that. Therefore, the audit of WorldCom did not serve its purpose. However, the audit of Hikma was carried out as per auditing standards and performed all the required checks before the unqualified audit opinion was issued.

Critical Evaluation and Comparative Analysis of The Role of Board of Directors, Governing Body and Internal Auditors of The Two Companies

Board of directors

The directors of a company play a crucial role in determining the success of the entity in meeting its financial reporting obligations. They have the main responsibility of ensuring that the financial statements of the company are able to provide useful decision to the users of the financial statements for their decision making. Hence, the directors are responsible for the quality of information that is presented in the financial statements of the company. Even though the directors are not expected to hold strong expertise in accounting, they should be involved in the process of financial reporting and should ask for explanations on the accounting treatment selected and challenge those accounting treatments which do not seem appropriate (ACCA n.d. b.).

The board of directors at WorldCom comprised of popular leaders and chief executives of eminent companies, and other eminent people who had held reputable positions in the professional career. However, even though the Board of Directors comprised of respectable personalities, there was a major failure on the part of the board of directors of WorldCom to effectively discharge their responsibility of protection of wealth of shareholders and to prevent mismanagement in the company (Hilzenrath 2003). Certain investigative reports made into WorldCom indicated that the board of the company did not exercise independent leadership and never questioned any act of the management. The directors of the company were mere "observers" and were not vigilant enough in identifying the high-level fraud that was taking place in the company by its top executives (Hilzenrath 2003). The directors never questioned or challenged the information that was presented to them and did not denote towards their role in the company. On the other hand, the board of Hikma acted independently and carried out an assessment of the risk management framework of the company (Hikma n.d.). The BOD of Hikma pharmaceuticals comprised of Mr. Said Drawazah as the Executive Chairman and Mr. Siggi Olafsson as the CEO of the company (Hikma n.d.). The BOD of Hikma was diligent in carrying out their duties of protection of interests of shareholders and safeguarding the assets of the company. The BOD of Hikma maintained close supervision over the activities of its management and questioned and challenged the assumptions and estimates made by the management from time to time (Hikma n.d.).

Management

It is to be noted that the management or governing body of a company is responsible for preparation of financial statements of the company and also has the responsibility of ensuring that the internal control systems over the processes of the company are operating effectively. The top executives at WorldCom including its Chief Executive Officer Bernie Ebbers were involved in fraud and mismanagement which ultimately led to the downfall of the company and its bankruptcy (Thornburgh 2004). The company was able to keep up its market reputation by making a number of acquisitions ad was able to maintain high share prices. However, when the telecommunications industry faced a sudden collapse in the year 2002, the management of the company adopted aggressive accounting techniques so as to present a rosy picture to the investors and maintain its reputation in the market (Thornburgh 2004).

After this, the management of the company started recording fraudulent entries (that did not actually exist) so as to be able to reach a figure of earnings that were according to the expectation of Wall Street. The management of the company continued to report false profits for nearly thirteen quarters before the company went bankrupt. The fraudulent activities of the management were discovered by the internal auditors in the year 2002 which led to SEC investigations against the company and its ultimate bankruptcy. On the other hand, the management of Hikma strongly values the corporate ethics of integrity and transparency. The corporate governance at Hikma Pharmaceuticals is strong and is in compliance with the UK Corporate Governance Code (Hikma n.d.). There have been no instances of fraud or manipulation reported against any managerial personnel of the company. The independent directors of Hikma meet at least two times in a year and consider and review various matters related to the company.

Internal Auditors

The Internal auditors are responsible for providing an assurance that the internal controls, risk management procedures and governance of the company are appropriate and are operating in an effective manner. The internal auditor is responsible for looking into those matters which are significant for the long term existence and growth of the organization (Chartered Institute of Internal Auditors n.d.). The internal audit department at WorldCom was headed by Cynthia Cooper who was the first person who found about the huge fraud that took place at the Company (Buncombe 2002). The internal audit department of WorldCom was successful in discovering the accounting irregularities that had been carried out by the Chief Financial Officer of the company. It was identified by the internal auditor that the CFO had capitalized the operating expenses so as to present a good picture of the profitability of the company to the investors (Buncombe 2002). The financial statements of the company had overstated its earnings by $ 3.8 billion (Buncombe 2002).

Identification and Comparison of Accounting and Internal Control Risks of The Two Companies

Accounting Risks

The major accounting risk that existed at WorldCom was lack of “independence” in the board of director’s, audit committee and the compensation committee of the company.

The board and the audit committee of the WorldCom operated under the influence of its CEO Mr. Bernard Ebbers and the CFO, Scott Sullivan (Thornburgh 2004). The board of directors merely acted as silent approvers and there was unlimited power held by the CEO and the CFO. This had placed the CEO and the CFO in a position where they can penetrate accounting fraud within the company. The lack of diligence and independence of the board and the audit committee posed a serious threat to the credibility of accounting and reporting done by the company. The company made a number of acquisitions and the board of directors lacked oversight when approving the decision to make decisions that involved a billion of dollars (Thornburgh 2004). The company had made loans of around $400 million to the Chief Executive Officer, and all these loans were not provided against appropriate collateral as security for the loan (Thornburgh 2004). The company also made guarantees involving huge amounts for the benefit of the CEO, and there were no measures taken to verify the sufficiency of the collateral provided by Mr. Ebbers. All these facts indicated a lack of appropriate accounting controls and procedures in the accounting processes of the company.

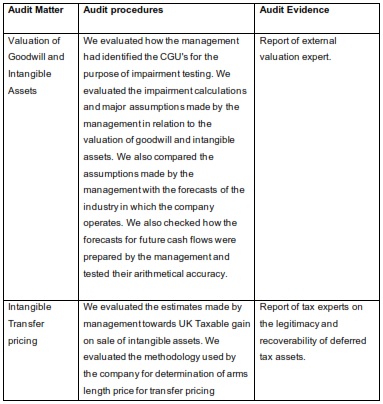

The most significant accounting risk that exists in the financial statements of Hikma Pharmaceuticals for the year 2019 is the risk of judgments formed by the management in relation to the valuation of goodwill being inappropriate. The company has presented goodwill of the value of $ 282 million and intangible assets of the value of $552 million in its financial statements as at 31st December 2019 (Hikma 2019). The management of Hikma Limited has made significant judgments in relation to the estimation of recoverable amount and value in use for the cash-generating units of the company (Hikma 2019). These amounts have been worked out by the management on the basis of their estimates regarding future cash flow forecasts, external market conditions and selection of suitable discount rate (Hikma 2019). Therefore, there is a high level of accounting risk involved in the valuation of goodwill and intangible assets of the entity. Any major errors made in these estimates relating to valuation of intangible assets could lead to a material misstatement in the financial statements of Hikma Pharmaceuticals for the year 2019.

Internal Control Risks

Internal control risks are those risks that arise due to weaknesses in the internal control system of the audit entity (Tarantino 2015). In order to identify the internal control risks that existed at WorldCom, it is important to look at the components of its COSO framework. The main components of the COSO framework are Control Environment, Risk Assessment, Control Activities and Monitoring (Westhausen 2010). The control environment at WorldCom was weak and this aspect of its control environment was indicated in the fact that the considering the large size of the company, the internal audit team had been provided with a few auditors only (Westhausen 2010). The Control activities were poor as the internal audit department did not have access to the complete information about the accounting system.

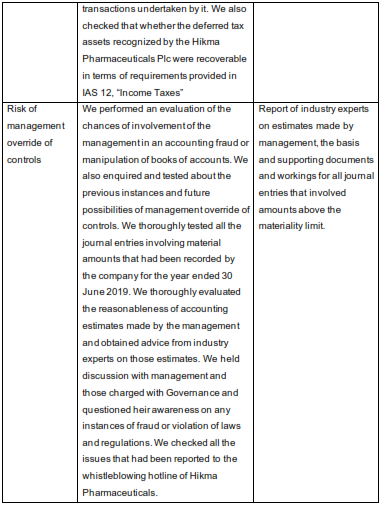

Hikma Pharmaceuticals is one of the leading pharmaceutical companies of the world that has its headquarters in London. Since the company deals in both the non-branded as well as licensed pharmaceutical products as well as licensed pharmaceutical items it faces a major internal controls risks that are specific to companies operating in the pharmaceuticals industry. The most important control risk that is faced by Hikma Pharmaceuticals is the risk of management override of controls and violation of the code of conduct and the ethical principles of the company.

Audit Risk, Audit Procedures and Audit Evidence for Hikma Pharmaceuticals for The Year 2019

Audit Risk

Audit risk refers to the risk that auditor may express an incorrect audit opinion on the financial statements of the company (Anon 1989). It is used to denote the risk that the auditor may be unable to detect any material misstatement that may be present in the financial statements of the entity. The audit risk has been broadly divided into 3 categories – Inherent risk, control risk and detection risk. Inherent risks are those risks which do not arise due to a weakness or inefficiency in the internal control system of the company. These risks are inherent owing to the level of complexity involved in a particular type of transactions or due to high level of judgments that are involved in the relation of classification, valuation and measurement of certain items that are presented in the financial statements of the entity. The International Standards on Auditing require that the auditor should follow the guidance provide in ISA 315, “Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment” and ISA 200, “Objective of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing” while making an assessment of audit risk (IFAC 2010).

We obtained a good level of understanding of Hikma Pharmaceuticals, its operating environment, internal controls, accounting processes as per the procedures prescribed in SA 315. In case of Hikma Pharmaceuticals, the inherent risks were determined by us as high owing to the number of significant judgments' that were involved in certain matters such as recognition and valuation of intangible assets (Hikma n.d.). Another major reason which has caused the determination of inherent risks involved in the audit as "high", is the nature and volume of transfer pricing transactions entered into by the company (Hikma n.d.). Moreover, the assets and liabilities of Hikma Pharmaceuticals, which are related to the acquisition of Columbus business involve a high degree of valuation risk (Hikma n.d.). We also determined the control risks to be high mainly due to gaps in the internal control processes of the company. The detection risk was determined to be lower as the size of audit samples that were selected by us were reasonable according to the size of the company and volume of transactions and owing to proper planning of audit such that no significant area of financial statements was missed out.

Audit Procedures and Audit Evidence

According to ISA 330, "The Auditor's Responses to Assessed Risks", an auditor is required to plan his audit procedures in such a manner that they are able to properly deal with the risk of material misstatement that was identified by him during the initial stage of the audit (ACCA 2010). The auditor is required to determine the nature, timing and scope of his audit procedures such that the auditor is able to collect sufficient as well as relevant audit evidence regarding the risks of material misstatement as per the risk assessment carried out by the auditor (ACCA 2010). The following audit procedures were carried out by us so as to respond to the inherent risks and control risks that were assessed by us:

Comparison of Audit Procedures of World Com and Hikma Pharmaceuticals

The audit procedures carried out by auditors of WorldCom were deficient and ineffective and were not capable of detecting even the most obvious misstatements that were present in the financial statements of the company. The audit procedures for WorldCom did not involve sufficient checks. Mr. Arthur Anderson was the external auditor who was responsible for carrying out an external audit of WorldCom (Ashraf 2011). The auditor procedures carried out by the external auditor were inadequate and the auditor was negligent in the performance of their duties. The external auditor did not tests the control environment at WorldCom, the gaps in internal controls and made no attempt to find out about instances of management override of controls and placed excessive reliance on internal controls at the company (Ashraf, 2011). The audit procedures carried out by the external auditor at WorldCom were limited to testing of account balances and did not identify major weaknesses in the internal controls that led to major accounting frauds by collusion of top management executives (Ashraf 2011). As a result, the auditors of WorldCom were unable to identify the fraudulent accounting adjustments in relation to the recognition of operating expenditure as capital expenditure.

The nature and extent of audit procedures carried out at Hikma Pharmaceuticals were in sharp contrast to the audit procedures carried out by the auditors of WorldCom. In relation to the audit of Hikma Pharmaceuticals, the control environment and operating effectiveness of controls were tested thoroughly. In addition to this, those areas which involved significant judgments were tested thoroughly so as to ensure that there was no possibility of management bias in the items presented in financial statements. The audit procedures for Hikma involved discussions with management about the possibility of fraud and error, detailed checking of all the journal entries that were posted by management and seeking of reports from external experts on matters related to the valuation of certain assets. Therefore, the audit procedures for the audit of Hikma were foolproof and were capable of identifying any weaknesses in internal controls and material misstatement that could be there in its financial statements.

Limitations of Audit Report of WorldCom

The following were the major limitations of the audit report of WorldCom

-

The audit report did not point out towards any accounting irregularity in the books of accounts even though the company had transferred millions of its operating expenses to capital expenses (Wharton 2002).

-

The audit report failed to point out towards the problems in the internal control structure of the company, the lack of oversight of the audit committee and the issue of management override of controls.

-

The audit report was not able to provide an indication of the problems faced by the company and did not provide any red flags to caution the investors regarding the ongoing financial issues and accounting fraud at the company which could lead to its bankruptcy (Wharton 2002). Instead, the audit report just provided an unqualified opinion which was not at all appropriate in those circumstances.

The Extending Audit Horizons

The case of WorldCom has made it evident that auditors have to look beyond the traditional audit practices and develop certain new auditing techniques that are capable of detecting any earnings management techniques and accounting fraud that could have been done by the management or employees of the entity. The auditors must perform certain effective analytical techniques and methods as described below so as to identify situations that could act as indicators of any potential fraud into the company:

-

Comparison of trends within the entity with other companies operating in the same sector or industry. The auditor should check whether the percentage of provisions for bad debts are similar, whether the terms of leases are similar or there are major variations.

-

Reviewing trends in cash flows and trends in earnings. If there is an opposite trend in these without any solid clarification/justification, this is an indication that the accounts of the company may have been manipulated (Wharton 2002).

-

Look for any events or incidents that could act as warning signs – disagreement between the company and its auditors, termination of any official of the company under questionable circumstances, change in lawyers etc.

References

ACCA (2010) ISA 330 and Responses to Assessed Risks. [online] available fromhttps://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-exams-study-resources/f8/technical-articles/ISA330-responses-assessed-risks.html#:~:text=ISA%20330%20requires%20that%20the,%2C%20account%20balance%2C

%20and%20disclosure. [28 June, 2020]

ACCA (n.d.a) Evaluation of misstatements [online] available from https://www.accaglobal.com/in/en/student/exam-support-resources/professional-exams-study-resources/p7/technical-articles/misstatements.html

ACCA. (n.d.b) Directors Responsibilities for Financial Reporting [online] available from https://www.accaglobal.com/content/dam/ACCA_Global/professional-insights/Directors-responsibilities-for-financial-reporting/pi-Directors-Guide-to-Financial-Reporting.pdf [26 June, 2020]

Anon, 1989. Accounting, auditing & accountability journal (Online).

Ashraf, J ( 2011) The accounting fraud at WorldCom the causes, the characteristics, the consequences, and the lessons learned [online] available from http://etd.fcla.edu/CF/CFH0003811/Ashraf_Javiriyah_201105_BSBA.pdf [28 June, 2020]

Buncombe A (2002) Directors asked how they failed to spot fraud [online] available from https://www.independent.co.uk/news/world/americas/directors-asked-how-they-failed-to-spot-fraud-130906.html [27 June, 2020]

Chartered Institute of Internal Auditors (n.d.) What is internal audit? [online] available from https://www.iia.org.uk/about-us/what-is-internal-audit/#:~:text=The%20role%20of%20internal%20audit,control%20processes%20are%

20operating%20effectively.&text=We%20must%20be%20independent%20from,organisation

%3A%20senior%20managers%20and%20governors. [26 June , 2020]

Hikma (n.d.) 2019 Annual Report [online] available from https://www.hikma.com/media/2733/2019-full-ar.pdf [27 June, 2020]

Hilzenrath D (2003) 'The company's directors were all too often a passive rubber stamp for management and especially Mr. Ebbers.' [online] available from https://www.washingtonpost.com/archive/business/2003/06/16/the-companys-directors-were-all-too-often-a-passive-rubber-stamp-for-management-and-especially-mr-ebbers/05f02228-86fd-43a6-bb99-1a01bd38fd90/[27 June, 2020]

IAS Plus.com (n.d.) IAS 12 — Income Taxes [online] available from https://www.iasplus.com/en/standards/ias/ias12 [28 June, 2020]

IFAC (2009) International Stanadard on Auditing 315 [online] available from https://www.ifac.org/system/files/downloads/a017-2010-iaasb-handbook-isa-315.pdf [28 June, 2020]

Investegate (2019) Hikma Pharmaceutical (HIK) [online] available from https://www.investegate.co.uk/hikma-pharmaceutical/rns/annual-financial-report/201904151223482242W/ [27 June, 2020]

Mortura Laura-Alexandra, 2017. Analysis of financial position in determining the general inherent risk. Analele Universităţii din Oradea. Ştiinţe economice, 28(1), pp.433–442.

Tarantino, Anthony. "Beyond Segregation of Duties: Next‐Generation Techniques in Evaluating User Access Control Risks." Risk Management in Finance. Hoboken, NJ, USA: John Wiley & Sons, 2015. 219-32. Web.

Thornburgh, D (2004). A crisis in corporate governance? The Worldcom experience [online] available from http://www.klgates.com/files/tbl_s48News/PDFUpload307/10326/Corp_Gov.pdf [27 June, 2020]

Westhausen, H. (2010) The WorldCom Fraud Under A COSO Magnifier [online] available from https://www.fraud-magazine.com/article.aspx?id=2147483732 [27 June, 2020]

Wharton (2002) What Went Wrong at WorldCom? [online] available from https://knowledge.wharton.upenn.edu/article/what-went-wrong-at-worldcom/

Remember, at the center of any academic work, lies clarity and evidence. Should you need further assistance, do look up to our Audit and Assurance Assignment Help

Get It Done! Today

1,212,718Orders

4.9/5Rating

5,063Experts

Highlights

- 21 Step Quality Check

- 2000+ Ph.D Experts

- Live Expert Sessions

- Dedicated App

- Earn while you Learn with us

- Confidentiality Agreement

- Money Back Guarantee

- Customer Feedback

Just Pay for your Assignment

Turnitin Report

$10.00Proofreading and Editing

$9.00Per PageConsultation with Expert

$35.00Per HourLive Session 1-on-1

$40.00Per 30 min.Quality Check

$25.00Total

Free- Let's Start